VIE 的利润是如何转移给海外上市公司的?转移受哪些限制?「金融

![]()

壹、什么是VIE架构

很多创业者朋友近日致电我们(迅实资本),想要了解关于VIE架构的问题,尤其是“VIE架构下,利润是如何转移到境外公司”,对此,我们以本文作为统一解答。

对于上述问题,我们先做一个拆解,这个问题中由三个核心词:VIE架构、转移、境外公司。

根据这三个关键词,我们从概念上对该问题做一个基础的了解。

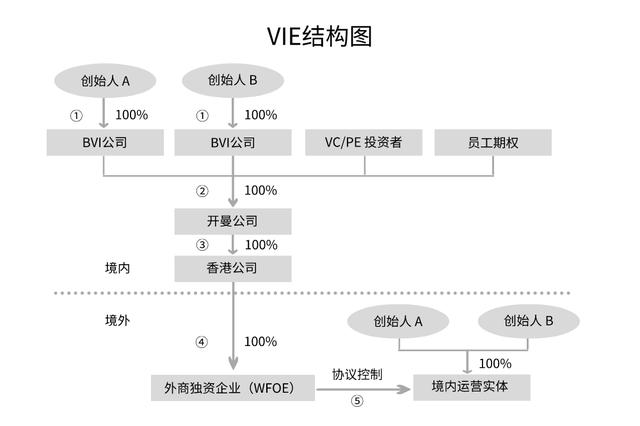

(一)VIE架构

VIE模式(Variable Interest Entities),直译为“可变利益实体”,即VIE架构,在国内被称为“协议控制”。

VIE是指境外注册的上市实体与境内的业务运营实体相分离,境外的上市实体通过协议的方式控制境内的业务实体,业务实体就是上市实体的VIEs(可变利益实体)。

(二)境外公司

VIE架构下,利润一般产生在境内的运营实体,境外的控股公司、香港公司及外商独资企业(WFOE)往往没有实质性的资产及业务运营,因此一般也不产生利润。

(三)转移方式

VIE架构下利润的转移方式:

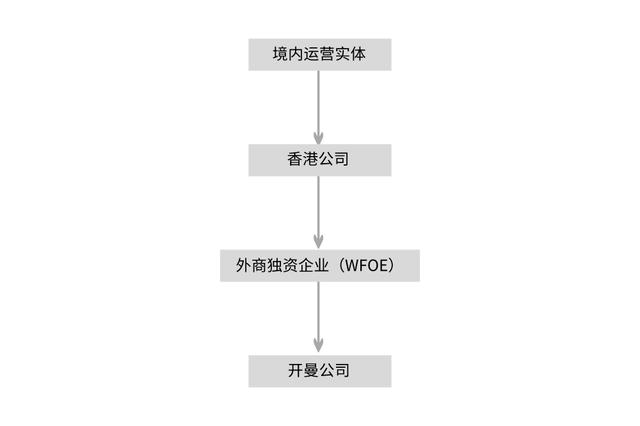

从境内运营实体 → 外商独资企业(WFOE) → 香港公司 → 境外控股公司。

WFOE是股权100%受控于香港公司,香港公司100%受控于开曼公司(境外控股公司)。所以,利润从WFOE到香港公司,并进一步从香港公司到境外控制公司,都是以“子公司向母公司”进行红利分配的形式完成的。

贰、利润转移的具体流程

我们需要明确一点,境内公司和WFOE之间并没有股权控制关系,它们之间是通过VIE协议实现两者的联系。

因此,从境内运营实体产生的利润,也是通过VIE协议转移到WFOE。其中具体的流程是:

(一)咨询服务费

WFOE向境内运营实体独家提供技术咨询服务、企业管理等服务,并向境内运营实体收取咨询服务费。

以百度为例,2013年,境内运营实体向WFOE支付的服务费数额为其税前净利润的89%。

(二)IP许可使用费

在VIE架构下,往往将法律上可以由WFOE持有的IP(软件许可、Web版式许可、商标许可、域名许可等)许可给境内运营实体使用,并向境内运营实体收取知识产权许可使用费。

WFOE通过上述一种或多种方式从境内运营实体收到的费用往往能够占到境内运营实体利润的几乎全部,由此实现利润从境内运营实体到WFOE的转移。

一旦VIE架构形成,根据美国通用会计准则(US GAAP)或者国际会计报告准则,境外控制公司就能直接合并境内运营实体、WFOE及香港公司的财务报表,这往往是VIE架构财务上要实现的主要目的,而实践中,VIE架构的公司鲜有真正将利润实质性转移到境外控股公司的。

叁、利润转移限制

VIE架构下,利润转移的限制几乎就是在税收上。我们以新东方为例,具体情况如下:

1、学生报名,收营业税(营改增后收增值税)。

2、新东方中国(WFOE)收取特许权使用费等,收营业税(营改增后收增值税)。

3、新东方中国(WFOE)取得利润时,收企业所得税。

4、新东方中国(WFOE)向新东方上市公司(A公司)支付股息红利,收预提所得税。

由上可知,相对于一般的外商投资企业,VIE架构多交了一笔营业税;而相对于国内企业,VIE架构多加了一笔营业税和一笔预提所得税。

咨询顾问:大伟David

咨询热线:156 1833 0219(微信同号)

TCG

迅实资本作为长期从事中国企业境外上市的国际投资银行,已帮助大量的中国企业在境外成功上市,积累了丰富的案例经验。

主要业务包括香港、纳斯达克、英国、澳洲、荷兰等境外上市辅导顾问服务和投融并购服务。

公司的合作机构包括:平安金控、软银中国、启明、深创投、达晨、启迪、平安新投、中投中财、黑石集团、鼎晖投资、 启明创投、国药集团等。共与国内300余家投资机构、100多家基金公司、50余家会所律所、30余家券商、十余家银行以及多家金融产业园区有紧密合作。

团队的核心成员均具有多年跨行业的从业经验,在实业和金融领域积累了丰富的经验;团队拥有广泛的资源和渠道,力求为发展中企业提供一站式多方位的服务。

TCG

How is the profit of vie transferred to overseas listed companies? What are the restrictions on transfer?

I. what is vie architecture

Many entrepreneurs called us recently (Xunshi capital) to learn about the vie structure, especially "how profits are transferred to overseas companies under the vie structure". For this, we use this article as a unified answer.

To solve the above problems, we need to do a disassembly first, which consists of three core words: Vie structure, transfer and overseas companies.

According to these three key words, we have a basic understanding of the problem conceptually.

(1) Vie architecture

The vie model (variable interest entities, translated as "vie") refers to the vie structure, which is called "agreement control" in China. It refers to the separation of overseas registered listed entities and domestic business operation entities. Overseas listed entities control domestic business entities by agreement, and business entities are vies of listed entities.

(2) Overseas company

Under the vie structure, profits are generally generated by domestic operating entities, while overseas holding companies, Hong Kong companies and wholly foreign-owned enterprises (WFOE) often do not have substantive assets and business operations, so they generally do not generate profits.

(3) Transfer mode

Profit transfer mode under vie structure:

From domestic operating entity → WFOE → Hong Kong company → overseas holding company.

WFOE is 100% controlled by Hong Kong company and 100% controlled by Cayman company (overseas holding company). Therefore, profits from WFOE to Hong Kong companies, and further from Hong Kong companies to overseas controlled companies, are all in the form of "subsidiaries to parent companies" for dividend distribution.

II. Specific process of profit transfer

We need to make it clear that there is no equity control relationship between domestic companies and WFOE, and the relationship between them is realized through vie protocol.

As a result, profits generated from domestic operating entities are also transferred to WFOE through vie agreements. The specific process is as follows:

(1) Consulting service fee

WFOE provides exclusive technical consulting services, enterprise management and other services to domestic operating entities, and collects consulting service fees from domestic operating entities.

Take Baidu for example, in 2013, the amount of service fees paid by domestic operating entities to WFOE was 89% of its pre tax net profit.

(2) Intellectual property licensing fee

Under the vie structure, IP (software license, web format license, trademark license, domain name license, etc.) that can be legally held by WFOE are often licensed to domestic operation entities for use, and intellectual property license fees are charged to domestic operation entities.

In one or more of the above ways, fees received by WFOE from domestic operating entities can account for almost all profits of domestic operating entities, thus realizing the transfer of profits from domestic operating entities to WFOE.

Once the vie structure is formed, according to the US GAAP or international accounting reporting standards, overseas controlled companies can directly consolidate the financial statements of domestic operating entities, WFOE and Hong Kong companies, which is often the main purpose of the vie structure in finance. In practice, there are few companies with vie structure that actually transfer profits to overseas holding companies.

III. restrictions on profit transfer

Under the vie structure, the limitation of profit transfer is almost on tax. We take new Oriental as an example. The details are as follows:

1. Students apply for business tax (VAT will be charged after replacing business tax with VAT).

2. New Oriental China (WFOE) collects royalties, business tax (VAT after replacing business tax with VAT).

3. When New Oriental China (WFOE) makes profits, it is subject to corporate income tax.

4. New Oriental China (WFOE) pays dividends to New Oriental listed company (company a) and receives withholding income tax.

It can be seen from the above that compared with the general foreign-invested enterprises, vie structure pays an extra business tax; compared with the domestic enterprises, vie structure adds an extra business tax and an extra withholding income tax.

TCG

As an international investment bank engaged in overseas listing of Chinese enterprises for a long time, fast capital has helped a large number of Chinese enterprises to successfully list overseas and accumulated rich case experience.

Its main businesses include overseas listing advisory services and investment and financing M & A services in Hong Kong, NASDAQ, UK, Australia, Netherlands, etc.

The cooperative organizations of the company include Ping An financial holding, Softbank China, Qiming, Shenzhen Venture Capital, Dachen, Tus, Ping'an xintou, CIC Zhongcai, Blackstone Group, CDH investment, Qiming venture capital, Sinopharm group, etc. It has close cooperation with more than 300 domestic investment institutions, more than 100 fund companies, more than 50 Club law firms, more than 30 securities companies, more than 10 banks and a number of financial industrial parks.

The core members of the team have many years of cross industry experience, and have accumulated rich experience in industry and finance; the team has a wide range of resources and channels, and strives to provide one-stop and multi-directional services for developing enterprises.

咨询顾问:大伟David

咨询热线:156 1833 0219(微信同号)

Consultant: David

Hotline: 156 1833 0219(Wechat)

内容/排版:Ian&Leo 校稿/初审:Leo 美工/审核:Josh

— The End —

▽

高管团队

合作伙伴

客户精选

业务介绍